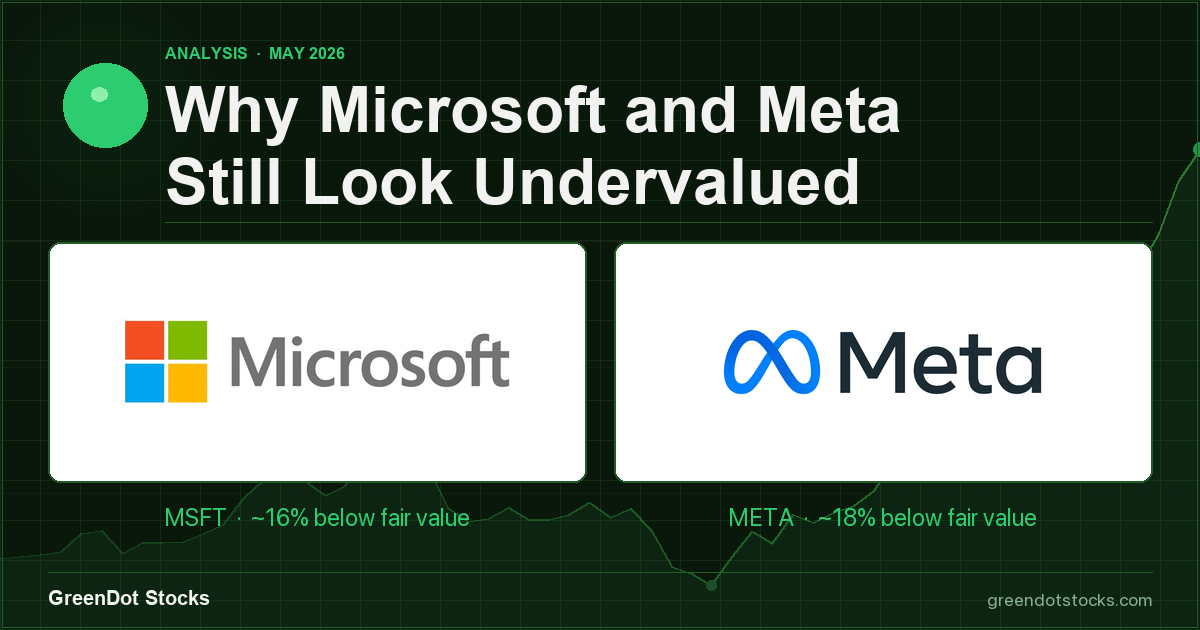

Microsoft (MSFT) and Meta Platforms (META) are two of the most studied companies on earth, which is why the setup is interesting. The market can see the strengths clearly, but it is struggling with the bill: both companies are spending at a level that makes even bullish investors uneasy, and both have enough complexity to keep skeptics engaged. On GreenDot Stocks, though, both still screen as green-dot businesses and both still look undervalued, with Microsoft trading about 16% below blended fair value and Meta about 18% below it. For investors willing to hold for three to five years, that gap looks more like opportunity than warning.

Why The Market Is Hesitating

Mega-cap tech does not usually get discounted because investors suddenly think the products are bad. It gets discounted when the path from heavy investment to future returns looks fuzzier than the headline story suggests.

That is the setup with Microsoft. The company just reported March-quarter revenue of $82.9 billion, up 18%, with Azure and other cloud services growing 40%. Microsoft Cloud revenue reached $54.5 billion, up 29%, commercial remaining performance obligation jumped 99% to $627 billion, and Satya Nadella said the AI business is now running above $37 billion in annual revenue. Yet the 10-Q also made clear why investors are uneasy: Microsoft Cloud gross margin fell to 66% from 69% a year earlier as AI infrastructure and AI usage ramped, Intelligent Cloud cost of revenue rose 47%, March-quarter property and equipment additions hit $30.9 billion, and the company disclosed another $196.6 billion of datacenter-heavy leases that have not yet commenced. Investors do not need to doubt Azure to worry that the return curve on all that spending could stay messy for longer than the bulls expect.

Meta has a similar tension. The company reported a strong first quarter: revenue rose 33% to $56.3 billion, ad impressions increased 19%, average price per ad increased 12%, and operating income grew 30% to $22.9 billion. But investors are reacting more to the forward bill than the current quarter. Meta raised its 2026 capital expenditure outlook to $125 billion to $145 billion, up from $115 billion to $135 billion, cited higher component pricing and more data-center investment, lost another $4.0 billion in Reality Labs, and again pointed to legal and regulatory headwinds in the EU and the U.S. The quarter's huge EPS growth was also helped by an $8.03 billion tax benefit, which makes it easy for skeptics to dismiss the headline even though the underlying operating performance was still excellent.

So the market's caution is understandable. Microsoft looks expensive if AI margins stay under pressure longer than expected. Meta looks risky if AI spending becomes another long-duration bet that takes years to fully monetize. The mistake is stopping there.

Microsoft Still Looks Like A Compounding Machine

The bullish case for Microsoft is not that spending will disappear. It is that the spending is being layered on top of one of the strongest recurring-revenue platforms in the world. Office 365, Azure, Dynamics, Teams, LinkedIn, and Copilot all feed the same enterprise relationship, which matters in AI because customers want compute, data, identity, workflow, and distribution already stitched together.

A company does not accidentally produce a $627 billion commercial remaining performance obligation balance. That backlog reflects deep commitments and strong forward visibility. The same quarter also showed Microsoft 365 Commercial cloud revenue up 19% and Azure up 40%, suggesting AI demand is showing up inside the installed base rather than in isolated pilots.

We try to capture what the market can miss when it fixates on capex. Microsoft still carries a current-year Rule of 40 score of 42.2%, a next-year Rule of 40 of 41.8%, and FCF-ROIC of 26.2%. That is a profitable, cash-generating platform still growing revenue mid-teens at massive scale. With the stock around $414 and the blended price target at $480.75, the valuation already assumes caution.

The real bear case is not that Microsoft is broken. It is that AI monetization will disappoint relative to today's hopes. That risk is real. But even if Copilot adoption unfolds more gradually (the opposite of what the metrics are telling us), Microsoft still owns the infrastructure, contracts, and customer relationships where that spending is likely to land. Over a three-to-five-year period, that looks more like patient compounding than speculation.

Meta Is More Than An AI Capex Story

Meta's undervaluation is even more striking because the operating business is still so strong. Investors often talk about Meta as if it were making a leap of faith into AI, but Meta is already monetizing AI every day through better ad targeting, better content discovery, and better engagement across Instagram, Facebook, and WhatsApp.

That is why the recent quarter deserves more weight than the usual "yes, but capex" reaction. Revenue was up 33%. Family of Apps operating income was $26.9 billion. Worldwide average revenue per person, or ARPP, rose 27% to $15.66. Cash flow from operating activities was $32.2 billion. Those are the economics of an advertising platform that is still widening its moat, not defending a shrinking franchise.

The market remains cautious because Meta's risks are obvious and uncomfortable. The 10-Q is full of them: pressure from the EU's Digital Markets Act, privacy and youth-safety litigation, dependence on advertising, ongoing Reality Labs losses, and an enormous buildout in infrastructure commitments. History matters, though, because Facebook has already survived several episodes that once looked existential: the painful shift from desktop to mobile, the Cambridge Analytica political-data scandal and the global backlash that followed, and the expensive metaverse detour that forced management into a more disciplined reset. None of those episodes were trivial, but each one showed that Meta can absorb a serious strategic or reputational shock and still rebuild growth. The numbers today argue that Meta is spending from a position of strength, not desperation. On our screen, Meta carries a current-year Rule of 40 score of 56.4%, a next-year Rule of 40 of 49.9%, and FCF-ROIC of 31.4%. The business is still growing 25.0% this year by the screen's measure, and even next year's expected sales growth of 18.5% is excellent for a company of this size.

Just as important, Meta's capex is attached to a machine that already earns extraordinary returns. If AI investment were being piled onto a weak advertising business, the skepticism would make more sense. But Meta's ad engine is still improving. Ad impressions are rising. Price per ad is rising. Family daily active people, or DAP, is rising. That combination suggests advertisers are still seeing value, which is the core engine that funds everything else.

At roughly $608.74 versus a blended price target of $718.41, the market is pricing in a lot of caution already. That caution may prove warranted in the next quarter or two if investors keep punishing rising AI budgets. Over three to five years, though, it is harder to argue that a company with Meta's scale, cash generation, and ad monetization power should trade at a discount to intrinsic value unless you think the core platform is structurally weakening. Recent results suggest the opposite.

The Better Question Is Time Horizon

For short-term traders, both stocks can remain frustrating. Microsoft may keep facing questions about AI payback periods and cloud margin pressure. Meta may keep facing questions about capex, regulation, and whether yet another giant infrastructure bet will spook the market.

For longer-term investors, the better question is whether Microsoft and Meta are building durable advantages that will matter more in 2028 than they do in the next earnings cycle. Microsoft looks positioned to capture AI spending across infrastructure, productivity, and enterprise workflows. Meta looks positioned to keep improving ad economics while using its scale to absorb investment levels smaller competitors cannot match.

| Attribute | Microsoft (MSFT) | Meta Platforms (META) |

|---|---|---|

| Current GreenDot Stocks read | Green Dot, Undervalued, +16.0% margin of safety | Green Dot, Undervalued, +18.0% margin of safety |

| What the market is worried about | AI capex, cloud margin pressure, AI monetization timing | Capex surge, regulatory risk, ad concentration, Reality Labs losses |

| Why the discount looks interesting | Massive recurring revenue base, $627B commercial RPO, strong Rule of 40 | 33% revenue growth, elite cash generation, AI already improving monetization |

That does not mean there is no risk. It means the market may be charging too much for risks that are real but manageable.

If you are willing to hold through noise instead of trading every guidance nuance, both names still look more attractive than recent sentiment implies.

If you want to find more stocks that combine quality, durable growth, and a real margin of safety, spend a little time with the GreenDot Stocks screener.